How to Start a Business in 9 Simple Steps

Our readers always come first

The content on DollarSprout includes links to our advertising partners. When you read our content and click on one of our partners’ links, and then decide to complete an offer — whether it’s downloading an app, opening an account, or some other action — we may earn a commission from that advertiser, at no extra cost to you.

Our ultimate goal is to educate and inform, not lure you into signing up for certain offers. Compensation from our partners may impact what products we cover and where they appear on the site, but does not have any impact on the objectivity of our reviews or advice.

Building a business from scratch can feel like an overwhelming task, especially when you have never done it before. But when you take it one step at a time and stick to a proven process, finding success can come much sooner.

Some of the links on DollarSprout point to products or services from partners we trust. If you choose to make a purchase through one, we may earn a commission, which supports the ongoing maintenance and improvement of our site at no additional cost to you. Learn more.

Thinking about starting your own business? You’re not alone. According to data from Babson college, two out of three American adults believe that entrepreneurship is a good career choice. With dissatisfaction in corporate America on the rise, many people are taking matters into their own hands and starting their own businesses. This trend only looks to continue with the younger generation; a recent Nielsen survey showed that more than half of people between the ages of 15 to 21 years old want to start their own business.

But as Johnston Community College points out, over 90% of entrepreneurs lack any formal business education. Of course, there’s more to starting a business than just book-smarts, but you will need a plan if you want your business to thrive. Below, you’ll find a step-by-step guide for starting your own business.

Step 1: Coming Up with Your Idea

Many business owners simply take their existing hobby and turn it into a side hustle, then build it into a full-fledged career. Others find themselves starting from scratch.

In Simon Sinek’s bestselling book Start with Why he emphasizes the need for business owners to understand the motivations behind their business. “People don’t buy what you do,” he writes. “They buy why you do it. And what you do simply proves what you believe.”

Finding your “why” might take some brainstorming. Need help getting started? Grab a sheet of paper or a whiteboard. Draw a line down the middle. In one column, focus on the needs of the world around you. Focus on questions like:

- What needs do I see in the world today?

- Are there any recent problems that need to be addressed?

- What businesses are currently trending — and why?

On the other side of your brainstorming sheet, write down things about yourself, such as:

- What am I passionate about?

- What unique knowledge base or skill set do I possess?

- How do I want to impact my community or world?

Write down as many ideas as you can. Ask for input from your social circle. Remember: there are no bad ideas, so don’t prejudge any response at this point.

Once you’ve filled both columns, draw connections between the “need” side and your “skill” side. What problem would you like to focus on? How are you uniquely equipped to meet that need?

For instance, your community might be lacking in a certain type of construction contractor or a particular type of restaurant. If you can fill these needs, you have the potential for creating a successful business.

Step 2: Validate Your Idea

Finding your business idea is one of the most important steps in starting a business (here’s a list of business ideas if you need some inspiration). But before you run out and print your business cards, it’s important to validate your idea. Basically, you need to know if your business idea will work.

Understandably, you may not exactly have an extensive budget for market research. You can start by performing some simple research, like:

- Reading about the market or industry in online trade journals

- Researching customer demographics through the Small Business Administration

- Learning more about existing businesses in your industry

- Talking to prospective customers (or even your family) about your business plan

- Testing out your product or service with a small group of customers

Ideally, you’ll discover that your idea is not only feasible but that it meets the specific needs of your target audience.

Sometimes you’ll discover that even though you have a good idea, you’re facing stiff competition from other businesses. If so, you’ll need to refine your business idea still further. What makes your future business unique?

Don’t be discouraged if you don’t get a lot of buy-in from your prospective customer base. Return to step 1, and use input from others to zero in on a specific need that your business can fill.

Related: 20 Best Business Ideas for New Female Entrepreneurs

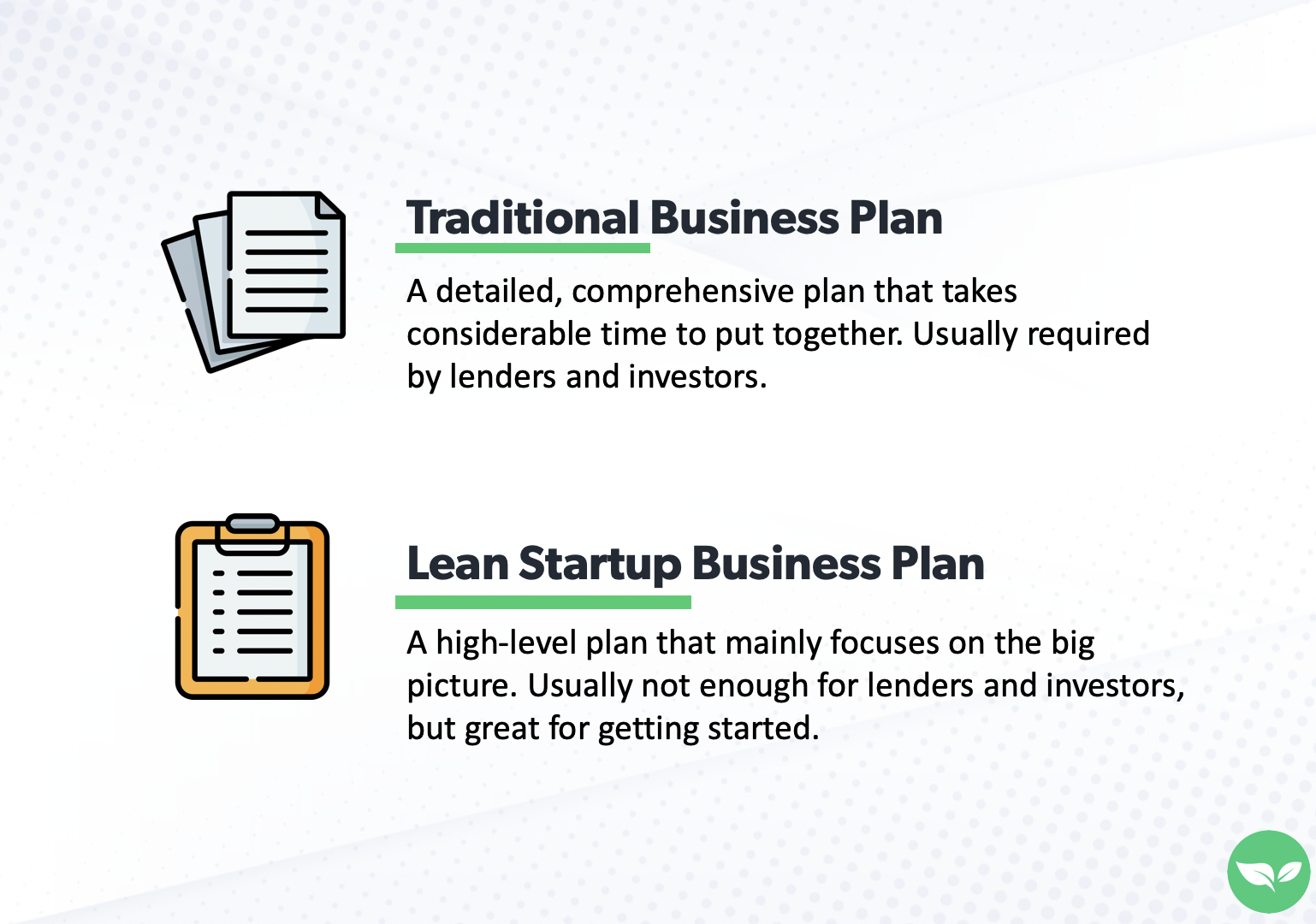

Step 3: Create a Business Plan

Next, you’ll want to write out your business plan. Don’t skip this step. A well-written business plan will help you stay focused on your specific business goals.

You can also use it to communicate data about your business to external audiences. If you’re communicating to potential investors or simply trying to secure a small business loan, you’ll likely be asked to present your business plan.

A traditional business plan will include the following:

- An executive summary highlighting key points from the rest of the document

- A description of your business, including your mission statement

- A description of your products or services

- Market analysis that shows your company has a viable market

- A marketing plan explaining how you intend to reach your target audience

- Your funding needs to show how much you’ll need to launch your business

- Financial projections, including milestones for earnings potential and growth

- An appendix containing additional market and industry data

You can also utilize what’s known as the “lean startup option,” which will contain the following elements:

- Your company’s value proposition

- A list of your services

- Primary activities

- Primary resources

- Business channels

- Target customers and customer segments

- Financial needs and cost structure

- Revenue streams and financial projections

If you need some inspiration, head over to the Small Business Association website, where you can learn more details and download some sample business plans.

It also might help to look at business plans for specific industries, such as:

You’ll likely refine your business plan over time, but putting your ideas down on paper provides a useful starting point that you can work from for the future.

Step 4: Build an MVP (Minimum Viable Product) or Service Offering

Once you’ve created your business plan, your next priority should be creating a “minimum viable product,” or MVP.

Think of your MVP as a prototype, simply designed to evaluate how well your final product or service satisfies the need you identified in the preceding steps.

Obviously, this will look different depending on the nature of your business. Your main priority should be bringing something to market fast. Ask yourself, “what minimum features do my product or service need to offer my target market?” Ignore the details for now — you can always fine-tune your initial design later.

Once you’ve designed your MVP, it’s time to launch. Again, it doesn’t have to be “pretty,” just functional. Learn from your customers’ experience:

- Did your product or service meet your customers’ needs?

- How might you improve the user interface or client experience?

- Are there design flaws that need to be addressed?

- How does your MVP measure up against competing products or services?

If you’re feeling shaky about this step, you might want to check out a few resources, including:

- A web agency that offers a detailed guide for developing an MVP

- An online calculator to determine the costs of your MVP

- An article from a software developer cataloging MVPs from top companies

Developing an MVP is an exciting step, as it allows you to see your company begin to take shape. Plus, it provides another opportunity to learn and refine your business before your official launch.

Step 5: Legal Steps

In order to operate your business, you’ll need to comply with existing business regulations. Many of these requirements vary by state, so you’ll have to do some research to determine your exact needs.

Find Your State’s Requirements

The Small Business Administration website provides resources to help you determine your legal requirements by state. Some of these requirements will also depend on how your business is legally structured. The purpose of these requirements is to comply with industry and safety regulations and ensure you pay taxes correctly.

Common requirements include:

- Articles of incorporation or operating agreements

- Financial statements

- Payroll taxes, workers’ compensation insurance, etc.

- Licenses and permits (for specific industries)

If you operate a business in certain industries, such as alcohol or firearms, you’ll need to comply with requirements regarding licenses and permits. You can find more information on the SBA website, which organizes these requirements by industry and state.

Apply for an EIN/Federal Tax ID

An Employer Identification Number, or EIN, is a 9-digit number used to identify your business for tax reporting. It’s also known as your federal tax identification number and functions as a kind of Social Security number for your business. You can get one through the IRS website for free.

Don’t delay. An EIN is a common requirement when applying for small business loans, and you’ll need one if you decide to hire employees.

Step 6: Financial and Accounting Steps

You now have a series of decisions to make about how to manage your company’s finances. It might seem daunting at first, but tackling these steps from the start will make everything much smoother for you down the road.

Choose Your Tax Entity

First, you’ll need to decide what business structure fits your company’s needs. The five most common types of business structures include:

- Sole proprietorships

- Partnerships

- Limited liability companies (LLCs)

- Corporations

- S corporations

If these terms sound like a foreign language, head over to this helpful article from Indeed.com. The structure you choose will influence your day-to-day operations and mitigate the amount of risk you take on when starting your own business.

Separate Your Business and Personal Finances

It’s not uncommon for business owners to sink their own cash into their company, especially when first starting out. But mixing your business and personal assets can create confusion during tax season and can jeopardize your personal assets if your business fails or gets slapped with a lawsuit.

This overlap is why you need to open a business bank account immediately. There are plenty of comparisons sites out there like Nerdwallet or Bankrate that can help you narrow down your options when it comes to choosing a bank for your business account.

For instance, some financial institutions offer unique tools for eCommerce companies, while others offer tools that can help retailers.

Additionally, while it’s possible to use an online bank, some business owners may prefer the convenience of a local, brick-and-mortar bank, especially when they need to make frequent deposits.

Choose Your Accounting System

How do you plan on managing your books? You basically have three options:

- Handling your books yourself with accounting software

- Hiring an accountant or bookkeeper

- Outsourcing your bookkeeping to a third-party accounting firm

Each choice has its strengths and weaknesses. While handling your own books makes sense when your company is in its infancy, you might find these administrative needs distract you from focusing on growing your business. Third-party firms can sometimes be a cheaper alternative to hiring an actual bookkeeper or CPA.

Related: Beginner’s Guide to Accounting and Reporting Blog Income

Consider Finding Financing

To fund your business, you might consider a small business loan or a business line of credit (LOC). A line of credit is often helpful for ongoing needs, while a loan can be helpful for startup costs and purchasing inventory and equipment.

Your bank may already have some options available and can likely help you navigate the requirements of an SBA loan program.

Step 7: Get Insured, if Necessary

Do you really need business insurance? If you have employees, your state may require you to carry business insurance. Also, if you’re renting retail space, it’s not uncommon for landlords to require you to carry insurance.

Likewise, some equipment manufacturers may prefer selling to companies that have an insurance policy. Plus, business insurance protects your assets in the event of a natural disaster, vandalism, or a lawsuit.

There are six common types of business insurance:

- General liability

- Product liability

- Professional liability

- Commercial property insurance

- Home-based business insurance

- Business owner’s policy

For more detail, the SBA website provides an overview of the advantages of each type of policy. The main question is whether your business involves enough risk to warrant a policy. It’s best to buy a policy when:

- You’re hiring employees

- You have a retail space visited by customers

- You work in a high-risk industry (e.g., construction)

- You rely on equipment, inventory, or resources that are costly to replace

Like any type of insurance, you may discover that it’s better to have it and not need it than to need it and not have it.

Step 8: Explore HR Needs

Depending on your business, you might choose to hire an extra set of hands or even a whole staff. The SBA provides some excellent resources on hiring employees, as does the employment site Indeed.com.

If you are just starting out as a one-person operation, you probably won’t need to worry about the items here yet, but it’s good to have them on your radar for when your business starts to grow and you need to bring on more help.

Here are just some of the things to consider when handling your human resources (HR) needs:

Benefits Offerings and Administration

Unless your staff is solely part-time, you’ll need to provide some type of benefits package. At a minimum, this includes health insurance, though many companies also offer retirement benefits and other financial incentives to attract and maintain top talent.

Legal Notices

Labor laws are constantly evolving. One of the ways employers must stay in compliance is by displaying legal notices in their workplace.

You can find more information about these notices and posters on the Department of Labor website. As the company owner, you’ll be responsible for staying abreast of changes in regulatory and compliance issues that impact your employees.

Tax Withholding

The Federal Insurance Contributions Act (FICA) requires that employers withhold the following taxes from their employees’ gross pay:

- 6.2% Social Security tax

- 1.45% Medicare tax (the “regular” Medicare tax)

- 0.9% Medicare surtax when the employee earns over $200,000

FICA also requires you to pay the employee’s portion of the following:

- 6.2% Social Security tax

- 1.45% Medicare tax

Failing to comply with these requirements can result in legal complications and penalties.

SOPs and SOGs

Employers will also be responsible for generating standard operating procedures (SOPs) and standard operating guidelines (SOGs) pertaining to employee conduct, job requirements, and workplace safety.

Options for HR

Like your accounting needs, you have three basic options for handling HR:

- Handling HR yourself

- Hiring an HR manager

- Outsourcing to an HR firm

As your business grows, it often becomes difficult to stay on top of changing regulations, which might lead you to consider farming your needs to a third-party or hiring your own HR manager.

Step 9: Finding Your First Customers

That old Kevin Costner movie got it wrong: just because you build it, it doesn’t mean your customers will come. While some industries can benefit from direct mailers to local residents, you’ll likely need to establish a strong web presence to effectively market your business. Focus on the following:

A User-Friendly Website

Start by building a modern, user-friendly website. Make sure that it looks good on a desktop computer as well as handheld devices.

You’ll want your site to contain basic information about your business, such as its location and the services/products you provide. E-commerce businesses will use their site to drive sales, while others might include contact forms to connect with potential clients.

Social Media Presence

Creating a profile or page on Facebook, Instagram, or other social channels can help you connect to a wider range of people.

If you have a specific post that you want to garner more attention, like a grand opening announcement, you can spend money and turn that post into an ad. As your business grows, you may delegate these responsibilities to an employee who can manage your social media accounts.

Email Marketing

Finally, develop an email list of regular customers. You can send them additional information, coupons, and other special offers to increase their loyalty and promote your business.

Related: 21 Inexpensive or Free Ways to Market Your Small Business

Bottom Line: Find Your Passions

If this sounds like a lot of work, it’s because it is. But few things are more rewarding than investing in an idea you’re truly passionate about. Your business venture, therefore, offers you something more than a paycheck. It gives you the opportunity to leave your mark on the world around you.