How to Get Your Spouse on Board with Paying Off Debt

Our readers always come first

The content on DollarSprout includes links to our advertising partners. When you read our content and click on one of our partners’ links, and then decide to complete an offer — whether it’s downloading an app, opening an account, or some other action — we may earn a commission from that advertiser, at no extra cost to you.

Our ultimate goal is to educate and inform, not lure you into signing up for certain offers. Compensation from our partners may impact what products we cover and where they appear on the site, but does not have any impact on the objectivity of our reviews or advice.

Getting out of debt is hard, but it can be even harder when your spouse isn’t working with you. If you want to get your partner on board with paying off debt, there are several ways to approach the conversation to make it productive.

Some of the links on DollarSprout point to products or services from partners we trust. If you choose to make a purchase through one, we may earn a commission, which supports the ongoing maintenance and improvement of our site at no additional cost to you. Learn more.

If you’d told 25-year-old me that I’d be debt-free by 28 and actually like talking about my finances, I would’ve said you’ve got me confused with someone else.

Back then I had no desire to pay off my $50,000 student loan or my $4,000 car loan. And when my fiance told me he wanted to pay off his $24,000 student loan, my response was, “Good luck!”

I wanted no part of budgeting, frugal living, or giving up the things that I thought made me happy.

But my now-husband wanted my support and participation, so he tried to get me on board. It didn’t take long before I was seeing things from his perspective. I saw paying off debt as something I needed to do to reach my own goals, and I admired him for his consistency and commitment.

And after two years of hard work and transforming my spending habits, we finished paying back $78,000 of debt; an accomplishment that was only possible because we worked together.

Why Working Together Is Better

You can go fast alone, but you’ll go further together. Being on the same wavelength as your partner can drive you further than you think possible. I initially thought it’d take us five years to pay off our debt; but because my husband and I were working together, we finished in two.

Science also knows the value of being in sync with your partner. The psychology behind teamwork is integral to NASA scientists working to send astronauts to Mars.[1] They know technology is important to get there, but understanding the dynamics of the small team of astronauts is critical to successfully completing a long-term mission.

You may not be trying to get to Mars, but paying off debt is still a long-term mission. Working together will make the journey easier.

6 Ways to Get Your Spouse on Board with Paying Off Debt

Getting out of debt is hard, but it can be even harder when your spouse isn’t working with you. If you want to get your partner on board with paying off debt, there are several ways to approach the conversation to make it productive.

1. Pick the right time to talk.

Choosing the right time to talk will put both of you in the right state of mind to have the most productive conversation. Allison Baggerly, the personality behind Inspired Budget, recommends scheduling a meeting on your calendar so you’re in agreement that it’s a good time for both of you.

If your spouse is hesitant or you think they may try to get out of it at the last minute, have something planned that’ll give them an incentive to show up. Maybe a bottle of wine or their favorite dessert — anything that will encourage their presence.

It’s important to know the wrong time to talk, too. Don’t bring up finances when you’re arguing about something else or in a time when either of you has heightened emotions. Your goal is to get your partner to associate paying off debt with the positive experiences, not negative ones.

Related: Money and Relationships: How to Merge Finances Without Any Drama

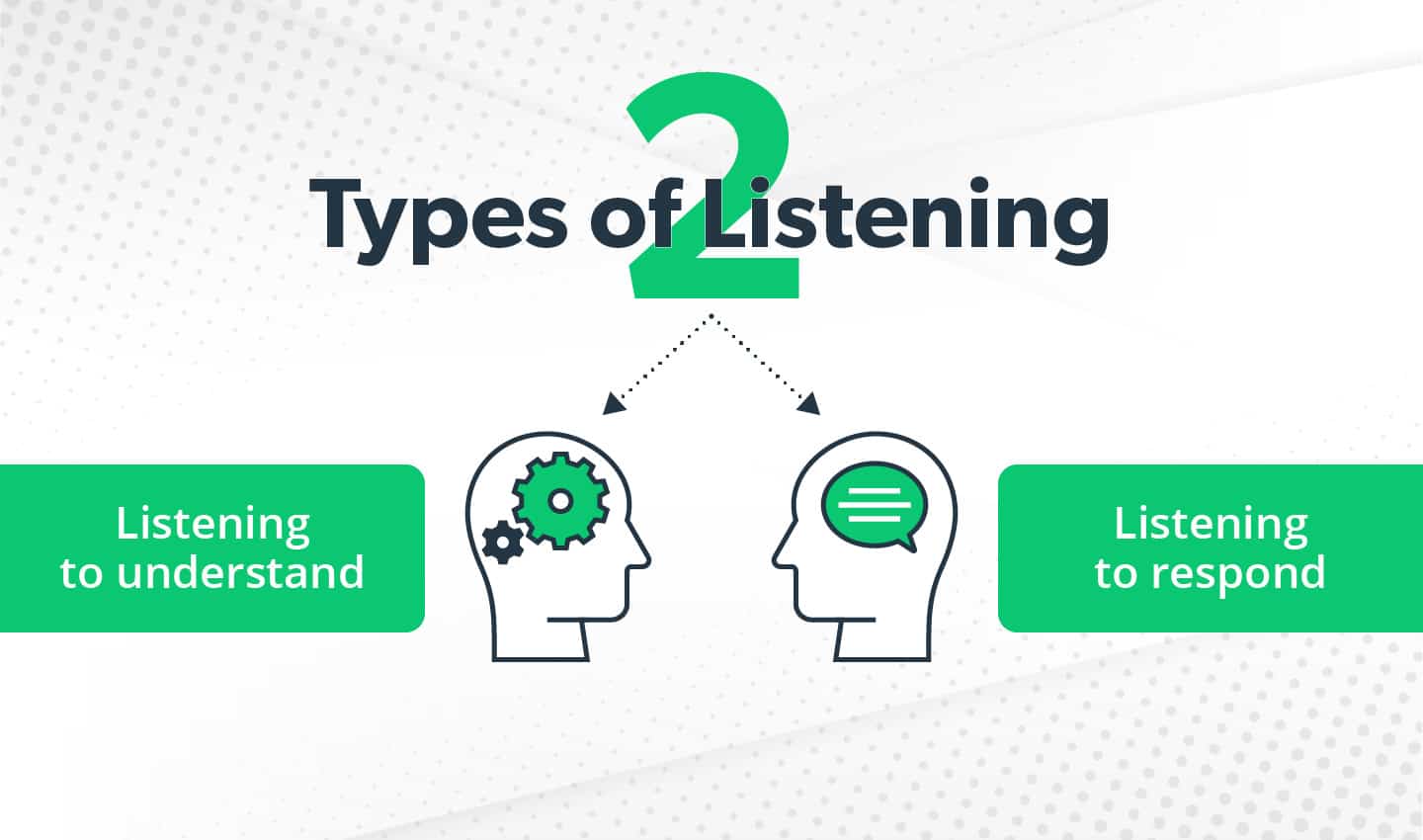

2. Listen more than you speak.

If you’ve put your opinions out there, then your spouse probably knows what you think about budgeting, debt, and saving money. But do you know how they feel? When you’re trying to get your partner on board with paying off debt, try to listen more and speak less.

Being excited about something can cause you to talk about it nonstop. Be aware of how often you’re bringing up financial topics so you don’t overwhelm or annoy your spouse. Then listen to what they say about things they want and frustrations with money or work.

Part of listening is paying attention to the things they’re not saying. For instance, try to take notice of their impulse purchases or how they behave when they’re paying for something. Noticing how they interact with money and spending can help you understand what they might be afraid to give up if they have to change their lifestyle.

3. Lead by example.

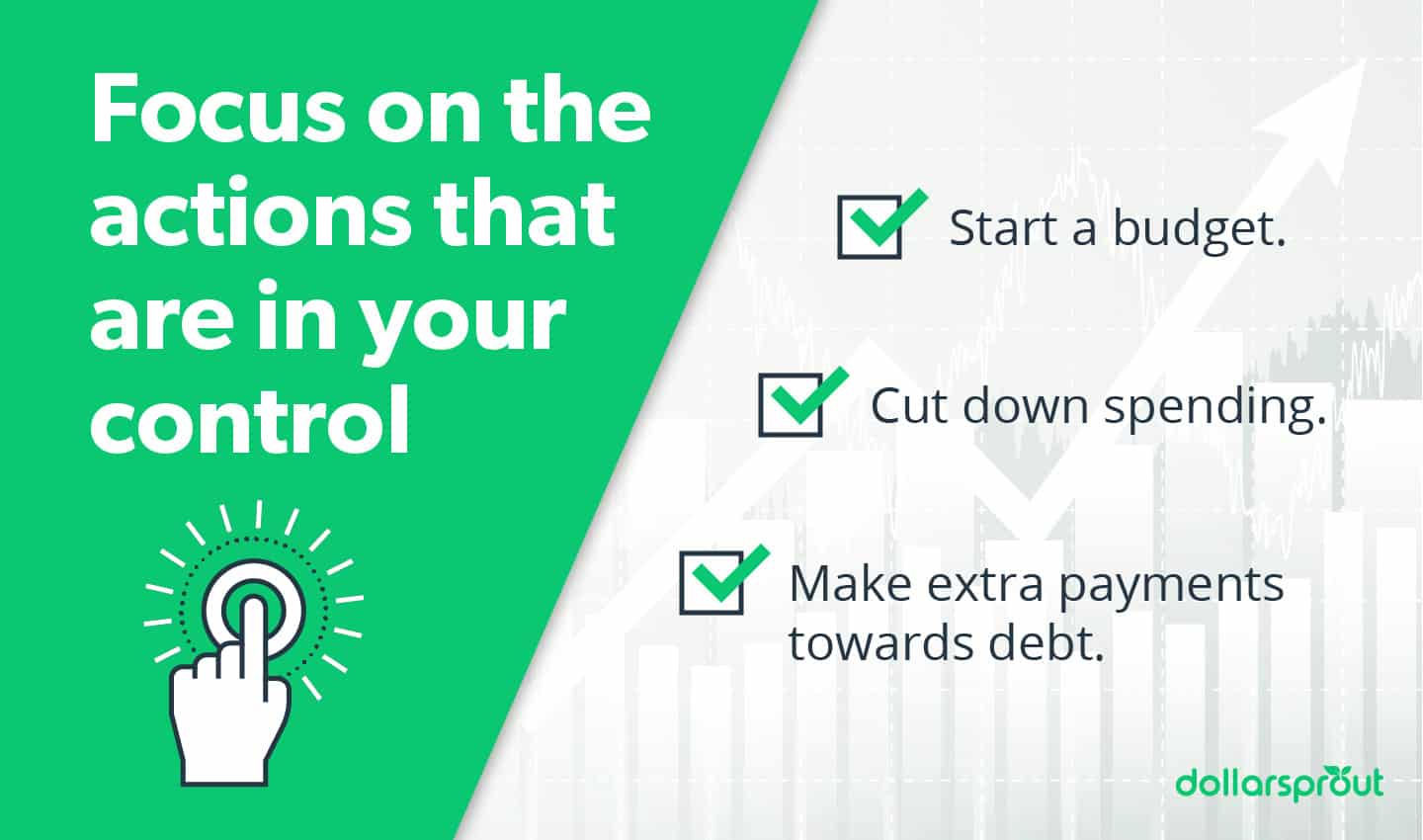

You don’t need to wait until your spouse is on board to make changes that improve your finances. Bettering yourself and celebrating small wins could inspire your partner to improve their own.

Of course, some things are hard to do when your spouse isn’t cooperating, so focus on actions that are completely in your control. Start budgeting your paycheck, cut down on your impulsive spending, and make extra payments toward debt when you can.

Don’t sugar coat your experiences to make it seem better than it is. Be honest when you’re struggling and reiterate why you’re committed even though it’s hard. This can be the most powerful example to motivate your spouse to join you.

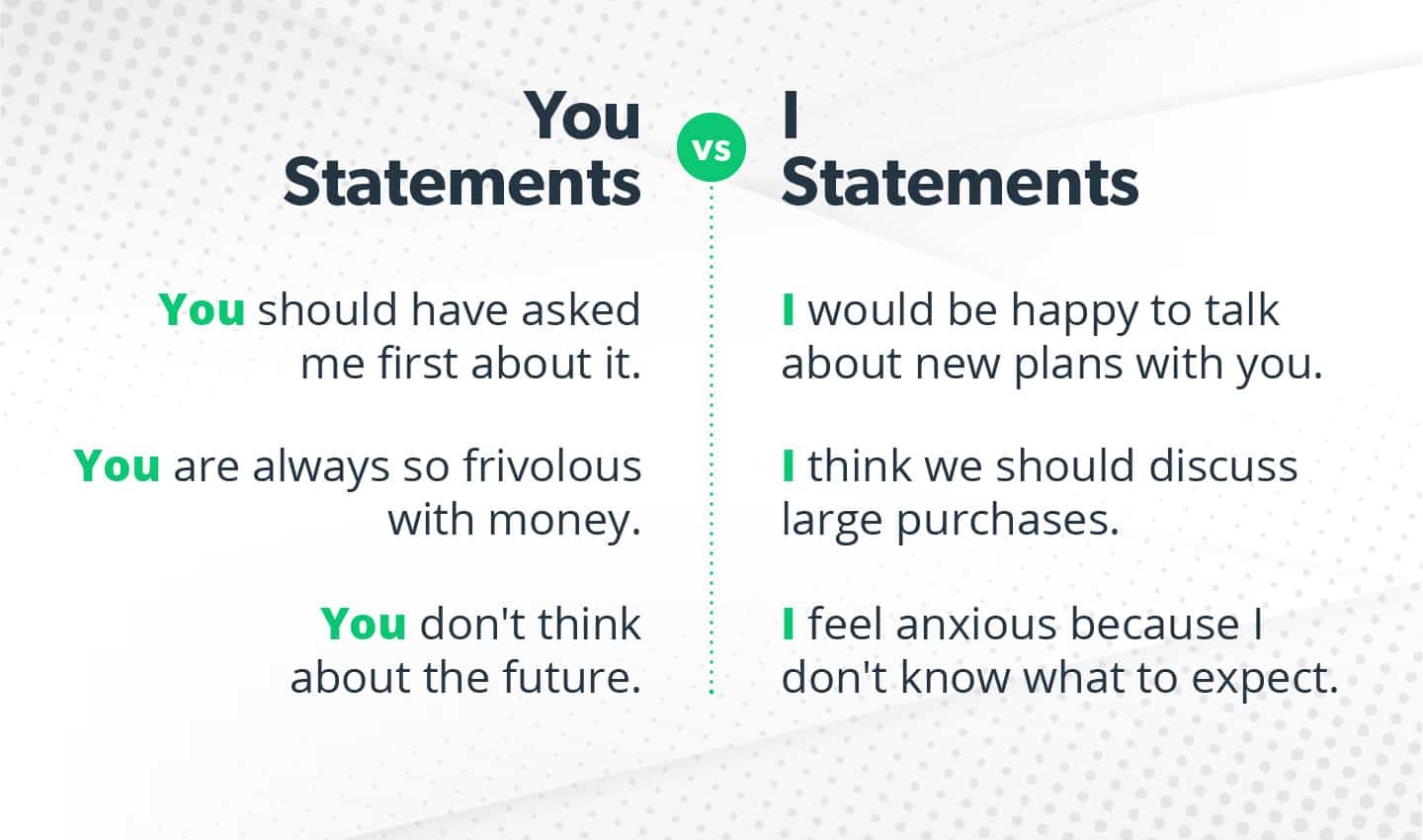

4. Speak with kindness.

Before you’re on the same financial page, your spouse may make a big purchase without consulting you first or ignore your efforts to talk about something money-related. In these instances, be aware of the tone you’re using to respond to them and speak with as much kindness as possible.

Speaking with kindness doesn’t mean being a pushover. You can still be mad, frustrated, or discouraged. It’s important to communicate those feelings, and the reasons for them, with a tone and language that’s not accusatory.

Accusatory language, even if it’s not used on purpose, can quickly cause your partner to shut down, become defensive, and kill any constructive conversation that could’ve been possible.

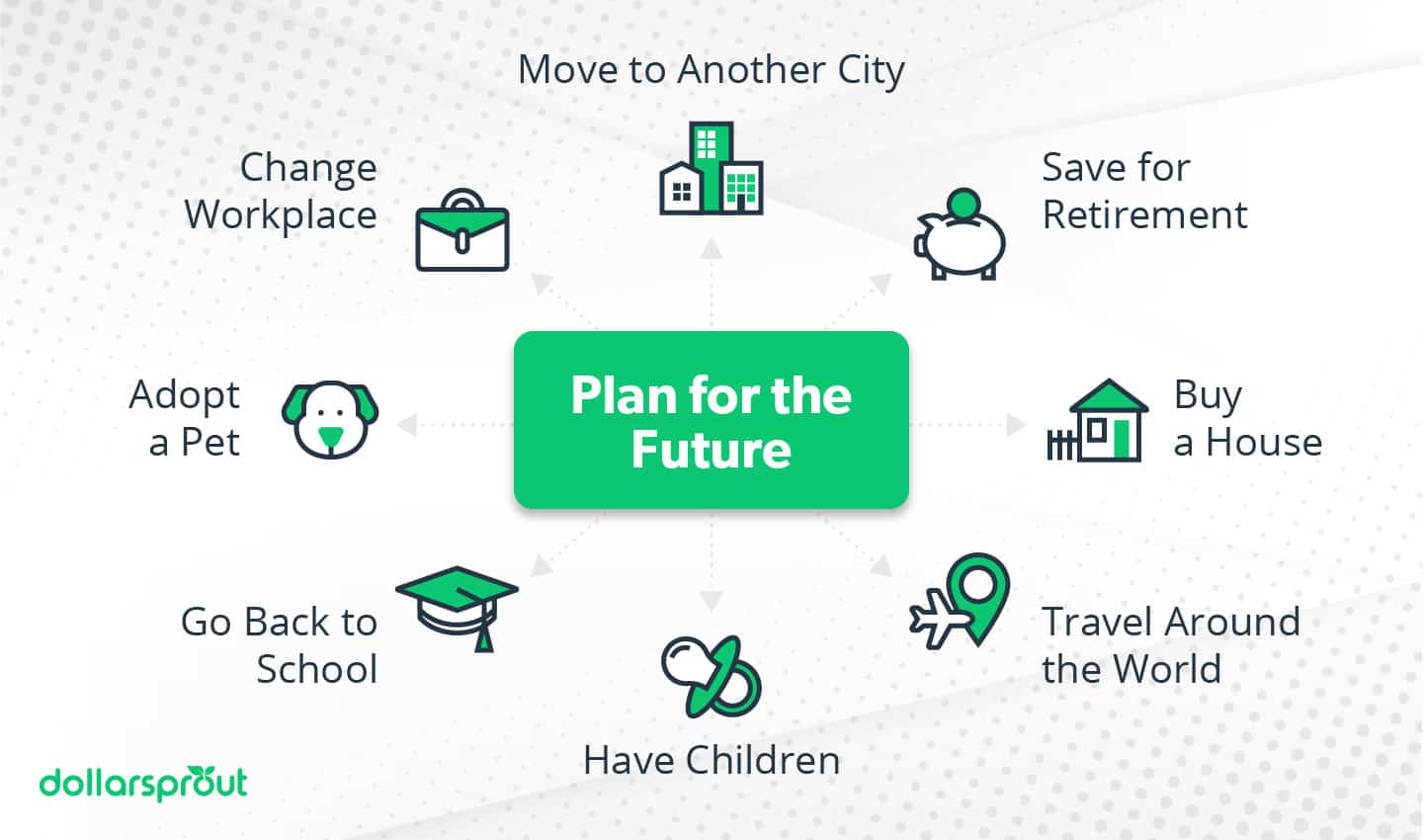

5. Ask forward-thinking questions.

If you want to encourage more conversations about finances, don’t interrogate your spouse with questions about their past spending. Molly Ford-Coates, a financial counselor and founder of Ford Financial Management, recommends asking questions that get them thinking about their future.

Everything we do involves some level of financial stability. Find out what your partner wants for their future and start planning how to get there. That plan will inevitably include a financial component, but don’t start with that. Discover your spouse’s “why?” and it’ll give them a reason to care about being debt-free.

6. Be patient.

Your spouse may not be on board with paying off debt on your timeline. Many people don’t want to think or talk about finances because they can be the source of debilitating anxiety, guilt, and shame.

There are usually deep-seated reasons why people don’t want to acknowledge their money problems. It may take time to get to the root of those issues and start pursuing debt freedom at the same pace. Avoidance isn’t necessarily a red flag; it’s just something you’ll need to have patience with and work through.

Related: Opinion: Married Couples Should Have Separate Bank Accounts. Here’s Why

What To Do If Your Spouse Won’t Join Your Efforts

It can be extremely discouraging when you and your partner’s goals don’t align. And it can be downright devastating when financial goals seem to contradict each other.

Don’t lose hope. Even if it’s clear you and your spouse will never be on the same page, or it at least looks that way right now, there are ways you can still work together.

Seek Counseling. Couples counseling isn’t a sign that your marriage is sick or broken. Rather, it’s a preventative measure to keep it healthy. All couples can benefit from occasional counseling sessions, but it’s essential for couples that are having difficulty seeing eye to eye on something.

Getting an outside perspective from a trained professional can give both of you perspective into what’s most important: your relationship.

If your partner is apprehensive, remind them that this isn’t reflective of them as a person, and you aren’t trying to fix them. Couples counseling is all about learning how to embrace differences and work with them.

Reality Check. If your spouse is in hardcore denial, they may need a reality check to what’s really going on because of your debt. Take inventory of all the numbers including the amount of your debt, how much you have saved for retirement, what you have saved for emergencies, and the impact those numbers have on your family’s future.

Lindsay Bryan-Podvin, licensed social worker and financial therapist, says to make your reality check as kind as possible. Avoid singling them out as the source of the problem, and be sure to cite your contribution to the current financial situation.

Stay Alert. Not every story has a happy ending. Unfortunately, financial infidelity is a common occurrence in relationships. If your spouse refuses to take responsibility for their finances, you have to be diligent in checking your shared and personal financial accounts and legally protecting yourself.

Look for unfamiliar bills, a regular occurrence of “surprise” packages, or a change in status on financial accounts like an account opened without your consent or your name being taken off a joint account. These could signify that your spouse is mishandling your money. You want to hope for the best, but it’s smart to prepare for the worst.

Related: Do Dave Ramsey’s 7 Baby Steps Actually Work?

Financial and Relational Security Is the Ultimate Goal

The point of paying off debt isn’t to have more disposable income or to simply say you’re debt-free. For most people, the real reason they want to have their debt paid off is to have more freedom and flexibility to live a life they love.

And the life you love undoubtedly includes your spouse. So remember that your family is more important than being debt-free. Keep living in a way that promotes your financial security and inspires your partner to join you. It may take time, but it’ll be worth the wait.