The 50/30/20 Budget Rule Explained (with Examples)

Our readers always come first

The content on DollarSprout includes links to our advertising partners. When you read our content and click on one of our partners’ links, and then decide to complete an offer — whether it’s downloading an app, opening an account, or some other action — we may earn a commission from that advertiser, at no extra cost to you.

Our ultimate goal is to educate and inform, not lure you into signing up for certain offers. Compensation from our partners may impact what products we cover and where they appear on the site, but does not have any impact on the objectivity of our reviews or advice.

Whether you’ve struggled to manage your personal finances consistently in the past or you’re looking to find a less time-intensive method, the 50/30/20 budgeting system is one option to consider.

Some of the links on DollarSprout point to products or services from partners we trust. If you choose to make a purchase through one, we may earn a commission, which supports the ongoing maintenance and improvement of our site at no additional cost to you. Learn more.

We all know someone who loves numbers.

They’ll spend hours poring over budgeting spreadsheets, examining the finer details of their investment accounts, and organizing the cash in their wallet by denomination.

For someone like that, being offered basic budgeting advice is like preaching to the choir.

For the rest of us, there’s the 50/30/20 budgeting system.

Whether you’ve struggled to budget consistently in the past or you’re looking to find a less time-intensive method, the 50/30/20 might be the approach you need to finally make it all click.

What Is the 50/30/20 Budget?

The 50/30/20 system was designed to make budgeting more accessible to people who get overwhelmed by complicated spreadsheets and budgeting apps. It was popularized by Senator Elizabeth Warren in her book All Your Worth: The Ultimate Lifetime Money Plan.

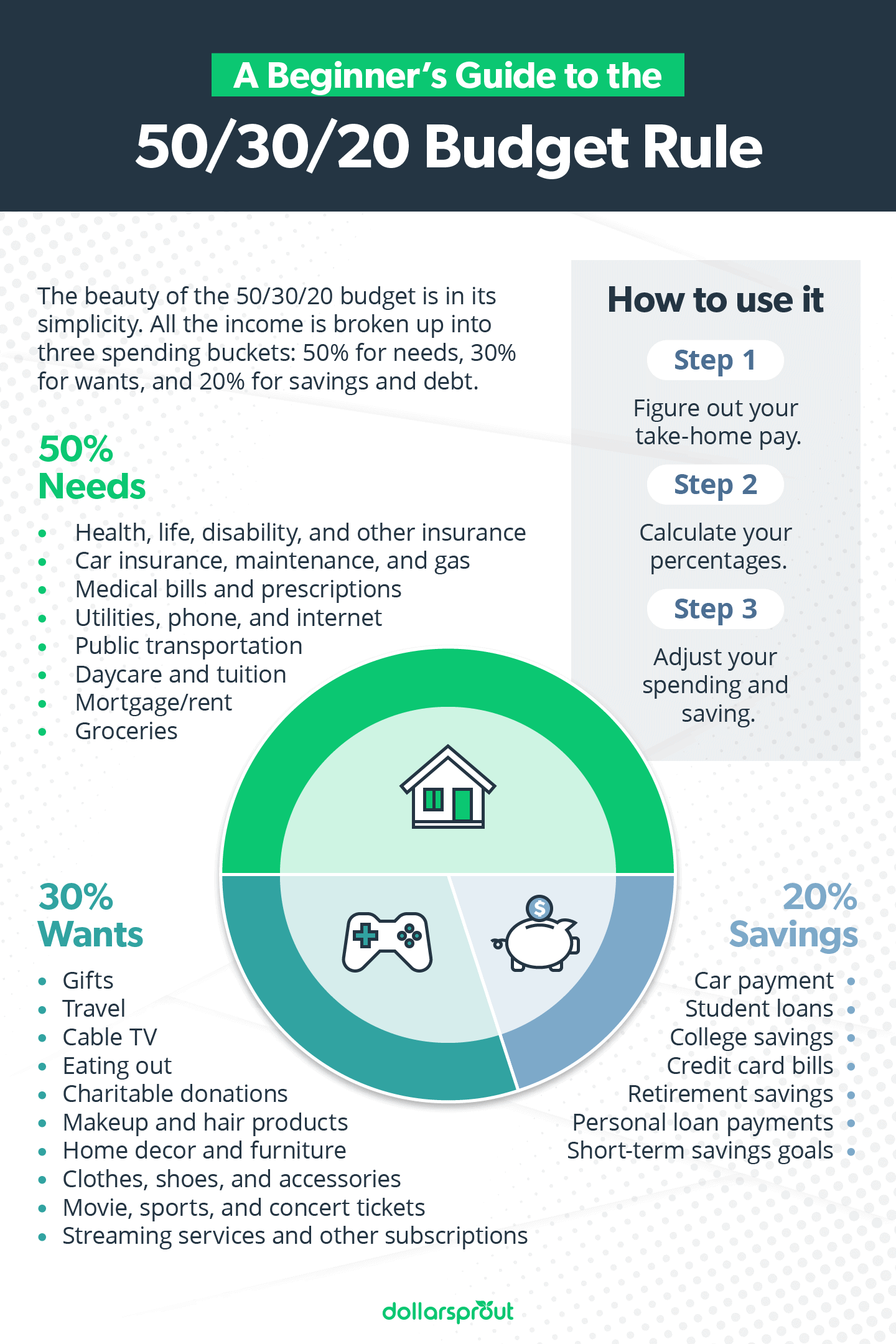

The beauty of the 50/30/20 budget is in its simplicity. It’s designed for people who want to track their spending without dividing each expense into a dozen separate categories.

Users of the system divide their transactions into just three buckets: needs, wants, and debt payments/savings. Spending is broken up into 50% for needs, 30% for wants, and 20% for savings and debt. Groceries would be in the needs group, makeup would be a want, and student loan bills would be a debt payment.

Here’s an example of what kinds of transactions might fit into each category:

Related: How to Make a Budget

Is the 50/30/20 Budget Right for You?

If you’ve tried to budget before and never quite got the hang of it, a 50/30/20 budget might be right up your alley. It’s like starting a fitness program. Jumping straight into a powerlifting routine might leave you sore and unmotivated, but starting with some light yoga will allow you to build a consistent exercise habit.

With the 50/30/20 system, you can start with the basics and get more complex as your financial literacy improves. It’s less of a specific system and more of an overarching philosophy.

It’s vague but flexible.

The 50/30/20 budget has become popular with people who struggle to categorize their spending. If you have separate line items for household goods and groceries, for example, a simple trip to Costco for saran wrap and cooking oil forces you to separate individual items from your receipt. With the 50/30/20, that kind of fussing is unnecessary.

The upside to this broader approach is that you spend less time figuring out how to budget each shopping trip. The downside is that you don’t really see where your money is going. If you need to cut some expenses from your “wants” category, the 50/30/20 budget won’t show exactly where you’re overspending.

It puts savings and debt on the back burner.

One of the reasons the 50/30/20 budget is popular is because it allows for 30% of a consumer’s income to go toward discretionary spending. Unfortunately, that doesn’t leave as much room for savings and paying off debt.

If your student loan payments make up 20% of your budget and you aren’t saving anything for retirement, the 50/30/20 approach could give you a false sense of stability. In reality, you’ll just be forced to play catch-up in the future.

Anyone who uses the 50/30/20 budget while paying off a significant loan balance should still try to save between 10 and 15% of their salary for retirement, even if that means shifting the spending ratio to allow for more saving.

It may not be a long-term solution.

The 50/30/20 is often suggested for beginners because it’s easy to use and set up. It also leaves a lot of room for variation, as long as you’re staying within the correct spending ratio.

But as a long-term budgeting strategy, the 50/30/20 budget might not hold up as well as a traditional line-item budget. That’s because the 50/30/20 split makes less sense above a certain income bracket.

When you’re making an entry-level salary, the 50/30/20 ratio is perfect. It allows you to enjoy your life and live comfortably while still prioritizing debt repayment and saving for retirement. But as your career progresses and your income increases, spending 30% of your income on discretionary items can be frivolous, and it can hold you back from reaching significant financial milestones.

Under the 50/30/20, someone making $80,000 a year after tax would have $2,000 a month for discretionary spending. That may be reasonable for someone with a robust social life and multiple hobbies, but many people would have to go out of their way to spend that much. As you approach upper-middle class, it makes more sense to follow a personalized budgeting system and devote more of your income to building a nest egg.

Related: How to Use the Cash Envelope System to Stop Overspending

How to Use the 50/30/20 Budget

There are three simple steps to creating and implementing a 50/30/20 budget spreadsheet.

Step 1: Figure out your take-home pay.

The first step in creating a 50/30/20 budget is to figure out your net income since that’s the figure you’ll be dividing from. Your net income is how much you take home after payroll taxes are deducted.

Look at your most recent pay stub to see what your take-home pay is. Even though your health insurance and retirement contributions may be deducted from your paycheck, you want to count these expenses as part of your budget.

If you’re self-employed, you’ll want to figure out your take-home pay after federal and state self-employment taxes. These will vary depending on your income and business expenses, so just use your best estimate.

People with irregular salaries, like salesmen working on commission or those with seasonal income, should use a realistically low figure when calculating take-home pay.

Step 2: Calculate your percentages.

First, make a list of all your transactions from the past month:

| Category | Amount |

| Rent | $775 |

| Electric bill | $50 |

| Water/gas bill | $60 |

| 401(k) Contributions | $100 |

| Car payment | $250 |

| Car insurance | $65 |

| Restaurants | $150 |

| Groceries | $350 |

| Health insurance | $95 |

| Gas | $115 |

| Cell phone | $45 |

| Internet | $55 |

| Lyft/Uber | $50 |

| Student loan payments | $250 |

| Netflix/Hulu | $30 |

| Clothes, shoes, and accessories | $100 |

| Makeup/haircare | $35 |

| Pets | $40 |

| Total: | $2,615 |

Then divide them into needs, wants, and savings/debt categories. Divide each of the three categories by your take-home pay to calculate your percentage, then compare those percentages to the ideal amounts. For this example, let’s assume a take-home amount of $2,700 per month.

| Needs | 50% | Wants | 30% | Debt/Savings | 20% |

| Rent | $775 | Restaurants | $150 | 401(k) Contributions | $100 |

| Electric bill | $50 | Netflix/Hulu | $30 | Student loan payments | $250 |

| Water/gas bill | $60 | Clothes, shoes, and accessories | $100 | Car payment | $250 |

| Car insurance | $65 | Makeup/haircare | $35 | ||

| Groceries | $350 | Pets | $40 | ||

| Health insurance | $95 | Lyft/Uber | $50 | ||

| Gas | $115 | ||||

| Cell phone | $45 | ||||

| Internet | $55 | ||||

| Total: | $1,610 | $405 | $600 | ||

| % of Income: | 60% | 15% | 22% |

Step 3: Adjust your spending and saving.

Like most people who create a 50/30/20 budget, you’ll probably discover that your percentages are out of alignment like the example above. Maybe you’re spending too much on your needs and not enough on your savings, or your wants category might be out of control. Don’t beat yourself up – it’s normal to find out your spending is a little off.

Examine where you need to make a change and explore options for how to save money in those categories. In this example, you can clearly see that the needs category greatly exceeds the 50% goal. To cut back, this person could reexamine their utility usage, negotiate with their cell and internet providers, or find a less expensive apartment.

You can also see in this example that student loan and car payments are mostly responsible for exceeding the 20% debt payment/savings category. In that case, it could be wise to make faster debt payoff a goal or try to pick up a side hustle.

The 50/30/20 Budget Simplifies Managing Your Money

Overall, consumers who like and stick with the 50/30/20 budget do so because of how simple it is. There’s little doubt on how to categorize expenses, and evaluating your spending can take just a few minutes each week.

The 50/30/20 budget has stuck around because it helps people who want to be responsible with their money but don’t like the restrictive nature of most budgeting systems.