Marrying Someone with Debt? Red Flags to Consider Before “I Do”

Our readers always come first

The content on DollarSprout includes links to our advertising partners. When you read our content and click on one of our partners’ links, and then decide to complete an offer — whether it’s downloading an app, opening an account, or some other action — we may earn a commission from that advertiser, at no extra cost to you.

Our ultimate goal is to educate and inform, not lure you into signing up for certain offers. Compensation from our partners may impact what products we cover and where they appear on the site, but does not have any impact on the objectivity of our reviews or advice.

Money and debt shouldn’t be taboo topics when you’re dating someone you want to marry. If you or your partner has debt, it's time to talk about it.

Netflix’s reality show, Love is Blind, had some standout moments. One of the most significant was the look on Matt Barnett’s face when his new fiance, Amber Pike, revealed she had $20,000 of student loans, no job, and no degree to show for it.

To many watching at home, Pike’s reveal wasn’t breaking news since 45 million Americans have student loan debt[1]. And three million of those borrowers have student loan balances upward of six-figures[2].

But it was a wake-up call to other couples who haven’t had “the debt talk” and begs the question, “how much debt is too much?”

Alli Williams, a financial coach who became debt-free in 2017 after paying off her $26,000 car loan, had to ask herself that question. She was dating the man she knew she wanted to marry. He still had a lot of debt. However, neither of them knew exactly how much.

When they finally did the math after getting engaged, they were both surprised at what they found. “When we finally added up all of Joe’s debt, the total was $154,000,” Williams said. “He thought it was closer to $100,000 so the total was a shock to both of us.”

Williams knew her fiance’s debt didn’t stem from being irresponsible and that he had every intention of paying it off once he finished school. But it still felt devastating. It took her a few days to recover from the shock. When she did, she had the same motivation that drove her own debt-free journey.

Money and debt shouldn’t be taboo topics when you’re dating someone you think you want to marry. Knowing what you’re getting into can help you prepare and plan for what’s to come. It can also help you identify red flags that could signal it’s time to leave.

How to Talk About Debt When You’re Dating

If you think you’re headed to the altar, it’s time to start talking about money. If you’re not sure yet, start as soon as you feel comfortable. You can change your approach depending on how long you’ve been together.

Start by framing the conversation around other topics.

Try not to jump right into the debt conversation with someone you don’t know. Williams waited until her fourth or fifth date to bring up finances directly. When you’re trying to gain an understanding for how the person feels about spending and debt, talk about things that involve but aren’t directly related to it.

For example, ask about their childhood. Did they go on vacation a lot? Did they attend public or private school? How extravagant were Christmases? Their opinions on how their parents spent money can give you an idea about how they view spending money now.

You can also ask questions about their education. What school did they go to? Did they get any scholarships? How often did they eat instant Ramen? Ask about their hobbies and what they like to do for fun now.

Be creative about how you approach the conversation to get a picture of how they view spending and saving.

Related: Should You Marry a Spender If You’re a Saver?

Don’t just talk about debt.

When you’re ready to dive deeper into the subject of money, don’t just talk about debt. Talk about income, retirement savings, things you value spending money on, opinions on charitable giving, and saving goals. This probably won’t be just one conversation. You might need to break it up over several weeks or months.

It’s OK if they’re not willing to tell you how much they make or their total amount of debt yet. Those numbers can be hard for some people to share and it might take some time before they’re comfortable enough to talk about specifics. But keep trying to have the conversation, and start watching for red flags.

If they aren’t willing to open up to you about general financial topics now, they’re unlikely to share specifics with you later.

Related: Money and Relationships: How to Merge Finances Without Any Drama

Get “financially naked”.

If the relationship is starting to get serious, you do need to sit down together and take a deep dive into your numbers before getting engaged.

“I tell my clients never to marry someone they haven’t gotten ‘financially naked’ with,” said financial counselor Christine Luken. “The couple should sit down with all of their bills and their credit reports and come clean about everything. If your partner has a huge amount of debt, it’s important to talk about how repayment will be handled once you’re married.”

You might think you know how much debt you or your partner have or assume you’re on track for retirement. But until you tally up the numbers, you won’t know for sure and it could lead to some significant revelations.

That’s what happened to Alli.

“For over 3 years I was mentally preparing to pay off $100,000. When we added up all of his debt the month before we started budgeting together, I felt frustrated when it was $54,000 more than we both thought,” she said. “I was mentally preparing for an amount that wasn’t even accurate.”

Red Flags to Look For Before Saying “I Do”

Debt itself isn’t a red flag, but there are circumstances that can indicate your partner has no intention of being open or honest with you, which could lead to them being financially unfaithful.

Your partner refuses to talk about money.

“One of the biggest red flags is the refusal to even have the money talk,” said financial counselor Molly Ford-Coates. “Both people need to be on the same page as to where they are right now and also where they want to go in the future.”

Entering into a marriage without knowing how much debt your spouse has will quickly break down trust no matter how big or small the debt is. If you’re engaged and your partner is still unwilling to share that information, it’s a big red flag.

Ford-Coates says there could be several reasons why the person doesn’t want to talk. They may be hiding something, feel embarrassed by their lack of financial literacy, or have a mindset that “everything will work out.”

You can work around these roadblocks by talking about your own shortcomings or insecurities when it comes to money and debt. You can even share inspiring debt payoff stories they might be able to relate to. But if you keep trying and your partner still refuses to open up beyond the surface level, it may be the sign of a deeper problem.

You can’t reach a compromise.

You probably won’t agree on everything money related, and that’s OK. But both of you should have a willingness to compromise. If your partner refuses to reign in their spending, pay off debt, or make any financial changes, don’t expect to change their mind after you’re married.

Consider seeking premarital counseling to get to the bottom of why your partner won’t change. If they still refuse, you might need to reevaluate if what you’re asking is important enough to end the relationship.

Related: How to Get Your Partner on Board with Paying off Debt

Your partner spends relentlessly.

Williams knew her fiance’s debt consisted of mostly student loans, a credit card, and a truck loan. But had it been due to multiple credit cards, personal loans, and merchandise financing, that’d be a different story.

If you see your partner going out a lot, ordering things and shopping constantly, or taking out debt without telling you, those are red flags that they might have a spending problem. And they don’t have to spend the money on themselves to indicate a problem. Don’t ignore the rounds of drinks at the bar, purchases for family members, or spending on you.

“Being on the receiving end of extravagant or luxurious gifts, dinners, or vacations feels wonderful, but when your partner’s spending doesn’t match his or her income, let that be the red flag of financial irresponsibility waving vigorously in front of you!” Ford-Coates said.

Related: Are You Addicted to Spending? Here are 5 Signs You Might Be

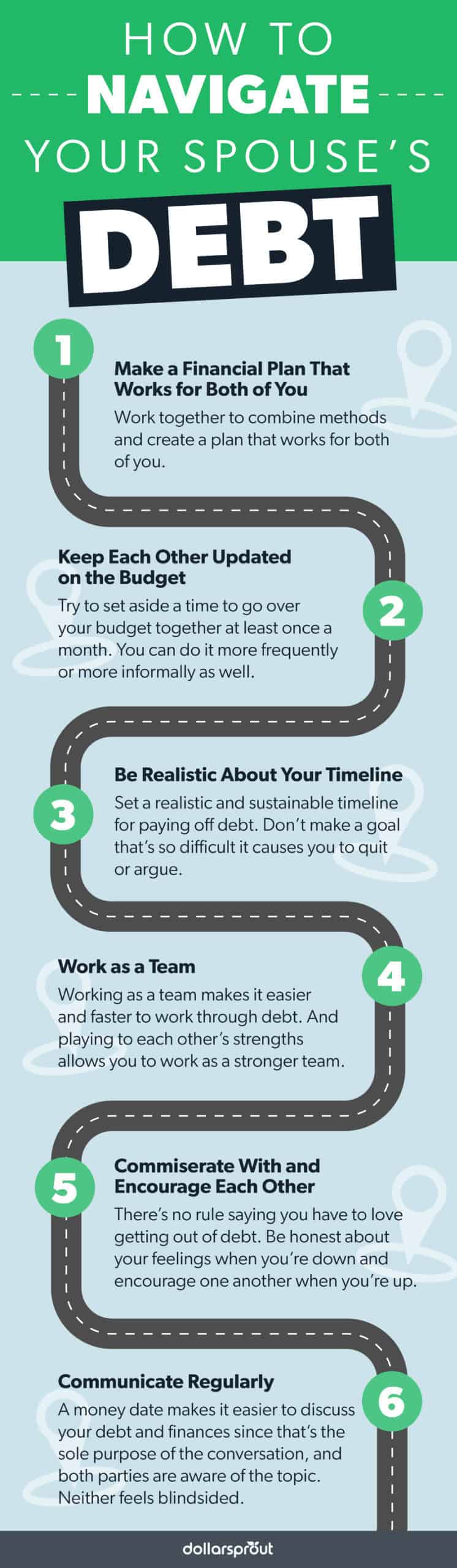

How to Navigate Your Spouse’s Debt

Once you’re married, you’ll begin, together, to tackle your spouse’s debt head-on. It won’t be easy, but there are some ways to make it simpler.

Make a financial plan that works for both of you.

One of you might want to use the debt snowball method to get out of debt while the other might like the debt avalanche. Work together to combine methods and create a plan that works for both of you.

Your financial plan shouldn’t just include how you’re getting out of debt, but also how you’ll invest, save, and spend on big purchases. It should also include a timeline for making a will and other estate planning essentials. One often overlooked part of a couple’s financial plan is their prenuptial agreement.

Not everyone needs a prenuptial agreement, but if one person is bringing significantly more debt into a marriage than the other, it’s wise to have one. Meet with a lawyer before you’re married and create a financial plan that will protect and satisfy you both.

If you’re already married, you can sign a postnuptial agreement to protect you from any financial harm that might result from your spouse’s debt. It will specify who is responsible for which debts in the event of a divorce and can also protect certain assets.

Keep each other updated on the budget.

A budget makes sure you know where your money is going. It helps you afford the things you need and directs you on how to change your spending to afford the things you want. In order to make that happen, you both need to be in agreement on your budget.

Try to set aside time to go over your budget together at least once a month. You can do it more frequently or more informally as well. That’s the approach Alli Williams takes.

She says that she and her husband don’t have monthly budget meetings, but they do check in with each other several times a month.

Related: How to Make a Budget in 7 Easy Steps

Be realistic about your timeline.

Set a realistic and sustainable timeline for paying off debt. Don’t make a goal that’s so difficult it causes you to quit or argue. Part of making your plan sustainable is incorporating rewards along the way, even if they slow down your timeline.

“We save and go to one Duke basketball game every year and we have kept my South Carolina football season tickets,” Williams said. “We realized we both value quality time together and experiences.”

These small luxuries motivate them to stick to their budget because they know they’re only spending money on things they truly value.

Work as a team.

Working as a team makes it easier and faster to work through debt. And playing to each other’s strengths allows you to work as a stronger team.

“[I] track our debt and I try to update Joe a few times a month on our progress. He is very supportive of our plan, but I manage our finances,” Williams said. “I am the one that is passionate about it and he trusts my decision making.”

Your spouse doesn’t have to love budgets to be on board with taking steps to pay off debt. Take inventory of what you each enjoy or are good at and stick to those strengths during your debt repayment journey.

Commiserate with and encourage each other.

There’s no rule saying you have to love getting out of debt. Be honest about your feelings when you’re down and encourage one another when you’re up. Knowing that you’re in this together and can share your feelings makes it easier to work through the days when being on a budget and paying off debt is just too hard.

“We will talk about how it sucks to put thousands to debt each month and we will talk about what we will do with that money once we are debt-free,” Williams said. “We keep each other motivated when one of us is feeling frustrated.”

Communicate regularly.

CPA and financial coach Allison Bishop also recommends scheduling a “money date” for couples who have a hard time talking about the subject. A money date makes it easier to discuss your debt and finances. Since that’s the sole purpose of the conversation, and both parties are aware of the topic, neither feels blindsided.

“One partner may be reluctant to have the conversation, but let them know that your financial situation is bothering you, and you’d really like to have their input about the next steps you can take,” Bishop said.

Related: How to Get Your Spouse on Board with Paying Off Debt

Don’t Let Debt Get in the Way of Love

Since combining their finances, Alli and Joe Williams have paid off over $44,000 of Joe’s debt. They’ve still got a long way to go but Alli knows marrying Joe was the right decision, debt or no debt.

“Since the beginning, I have said it is our debt, not his debt. We are a team and I am so blessed to have Joe as my husband,” Williams said. “Paying off six figures of debt is a long journey, but I wouldn’t want to do this with anyone else.”

Don’t wait to start paying attention to potential red flags and have hard money conversations. It’s worth it, especially if you love the person. As long as you’re on the same page, work together, and trust and rely on each other’s strengths, you can overcome any amount of debt.