Debt-to-Income Calculator

Our readers always come first

The content on DollarSprout includes links to our advertising partners. When you read our content and click on one of our partners’ links, and then decide to complete an offer — whether it’s downloading an app, opening an account, or some other action — we may earn a commission from that advertiser, at no extra cost to you.

Our ultimate goal is to educate and inform, not lure you into signing up for certain offers. Compensation from our partners may impact what products we cover and where they appear on the site, but does not have any impact on the objectivity of our reviews or advice.

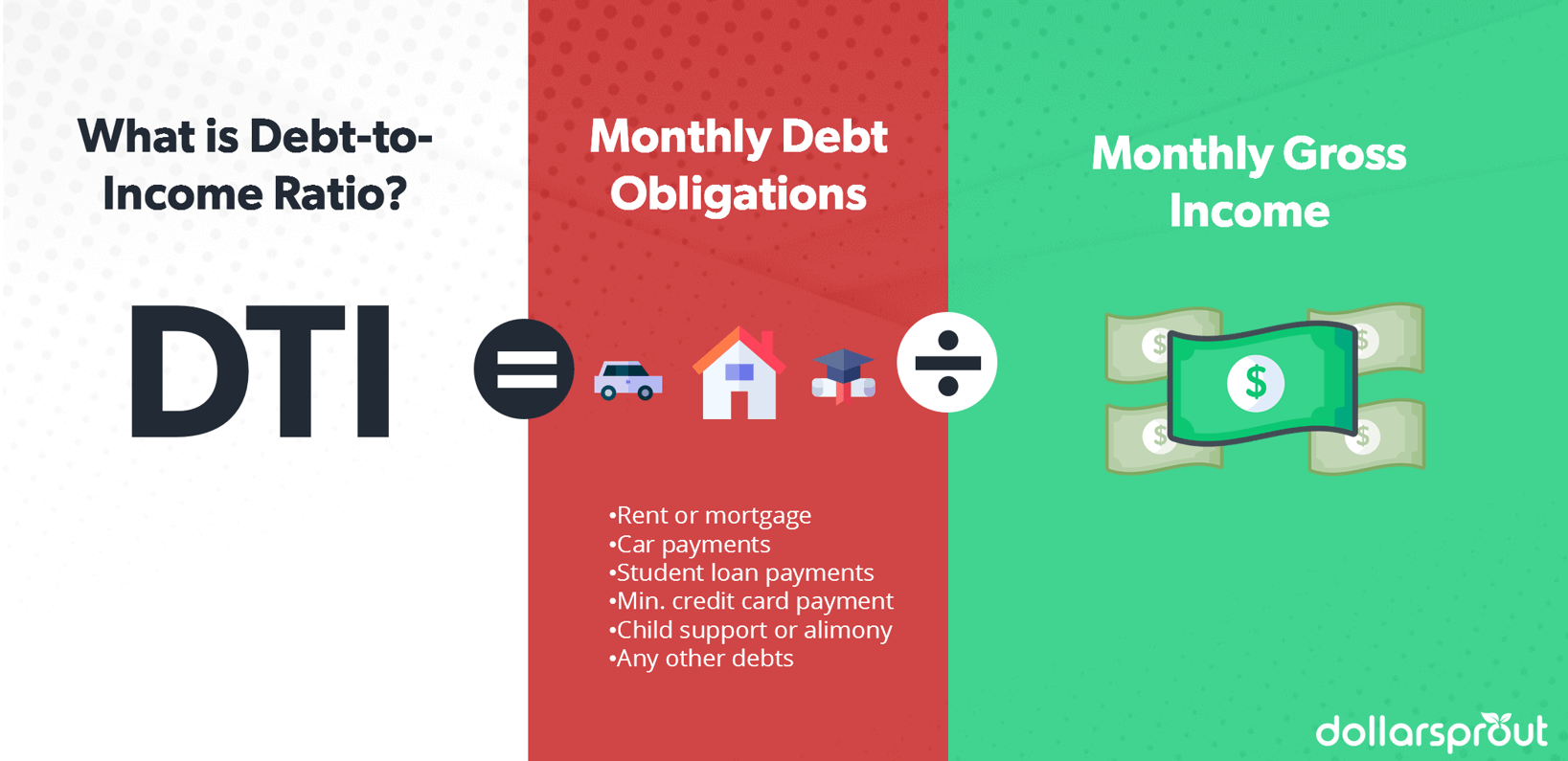

Your debt-to-income (DTI) ratio is one metric that lenders use to quickly assess your ability to handle debt. It provides a snapshot of your current debt load in comparison to your monthly income.

Use our Debt-to-Income Ratio Calculator below to determine what your DTI is:

How Most Lenders Look at DTI Ratios:

0-36%, ideal candidate for borrowing. In comparison to your income, your monthly recurring debts are at a manageable level.

36%-49%, you may qualify for a loan, but your terms won’t be favorable. It’s more risky to lend you money because you current debt commitments already eat up so much of your gross income. Some lenders may still approve you, but they will charge higher interest rates.

50% or more, you can’t afford to take on any more debt. You are unlikely to be approved for a loan because you are maxed out. After paying your monthly debts, you will have little to no money left over to save, spend, or handle emergencies.

We Recommend a Tougher Standard:

Remember, a lender’s primary goal is to make money off of their borrowers.

When a lender is assessing your financial health, they are taking a very limited look at your finances — they are not concerned with any other facets of your financial life, like savings goals, investing, or retirement planning. Lenders just want to know that you are going to be able to pay back your loan.

Because of that, we recommend a more conservative look at debt-to-income ratios:

0-15%, ideal. This gives you plenty of room to save for your future goals, and it also makes cash flow easier to manage each month. Even if your DTI is not this low yet, it’s a great goal to strive for.

15-36%, think very carefully before deciding to take on any more debt. Having a DTI in this range is how many people slip into living paycheck-to-paycheck. If you can, focus on lowering your DTI before taking on more debt.

Above 36%, lowering your DTI should be a top priority. By having so much of your income go towards monthly debt payments, it will be nearly impossible to make meaningful long-term financial progress.

Again, keep in mind that our recommendations are more conservative than what you will hear from virtually any lender. Debt is a big issue for a lot of people, and one reason for that is because lenders use guidelines that aren’t always in a consumer’s best interest.

What’s a Healthy Debt-To-Income Ratio?

From a lending perspective, a debt-to-income ratio under 36% is considered ideal, especially when it comes to getting approved for a mortgage. Most lenders will not approve a loan to you if it brings your DTI significantly over 36%. There are other factors that may affect your approval, though, including credit score, down payment, other assets that you have, and loan type.

Lenders will almost always prefer a low DTI to a high one, as that means you are more likely to pay your monthly debt obligations without any difficulty. Be sure to keep your other financial goals and obligations in mind, though, and don’t base your entire borrowing decision off of this one metric.

How Your Debt-to-Income Ratio is Calculated

Your DTI is the percentage of your gross monthly income (meaning, your income before taxes are taken out) that goes towards paying for your mortgage, rent, minimum credit card payments, car loans, student loans, and any other debt.

Items that are included:

- Monthly housing payment (either rent or mortgage)

- Monthly car payments

- Monthly student loan payments

- Monthly credit card payment (use minimum payment, even if you normally pay in full)

- Child support or alimony payments

- Any other debts

Items that are usually not included:

- Utilities payments

- Insurance premiums

- Groceries

Example:

Your monthly gross (pre-tax) income is $6,000. If the sum of all your monthly debts is $2,000, your debt-to-income ratio is 33%. This means that 33% of your pre-tax income goes towards your debts every month.

Two Flaws of the DTI Ratio: Taxes and Credit Card Minimum Payments

You may be thinking:

“A 36% DTI doesn’t sound too bad. That means I will still have 64% of my income left over each month to spend however I’d like.”

Unfortunately, that’s not how it works.

Your debt-to-income ratio is based off of your gross (pre-tax) income. Going back to our earlier example of $6,000, here is what a twice monthly paycheck would actually look like:

With a take-home salary that is 73.59% of your gross salary, things are starting to look much different.

Gross Monthly Salary: $6,000

Net Monthly Salary: $4,416

36% DTI: $2,160

Money leftover each month: $4,416 – $2,160 = $2,256

This means that, with a 36% DTI on a $6,000 monthly gross salary, you will have $2,256 that is left to spend on:

- Health, vision, dental insurance

- Auto insurance

- Groceries

- Entertainment

- Emergencies

- Savings goals

- Anything else life throws at you

In other words, having a 36% debt-to-income ratio at this salary means that for every dollar you earn, you will have just over 37 cents left over once taxes and debt payments are taken out. ($2,256 is 37.6% of $6,000).

Another quirk of the DTI ratio is that it only looks at your monthly minimum credit card payment. If you currently have a large amount of credit card debt but have a low minimum payment, your DTI ratio may give you a false sense of security and confidence in taking on more debt.

Credit card interest rates are usually among the highest rates of any lending product, which means they should always be a top priority for paying off. Using the minimum monthly payment as part of the basis for determining what additional debt you may qualify for is unwise in most situations.

How to Lower Your Debt-To-Income Ratio

Even if you are not currently looking to borrow money, it is a good idea to keep your DTI as low as possible. To lower your debt-to-income percentage, consider the following:

Pay down your current debts. If you currently pay the minimums on your credit card — or any other debt — your balance likely isn’t going down very quickly. The best way to accelerate your debt payoff is to get in the habit of paying more than the minimum monthly payments. Often times significantly more.

Downsize your living space. Your rent or mortgage is probably one of the biggest factors pushing up your DTI ratio. While it’s not practical for everyone, if you are able to move into a less expensive apartment or downsize your home, you can drastically reduce your DTI and free up more income for other financial goals.

Stop adding on more debt. Easier said than done, but your DTI ratio is not going to improve if your debt keeps increasing. If you need to, consider removing your credit cards from your purse or wallet.

Increase your income. More money coming in means your debt is easier to handle. Whether you ask for a raise, switch jobs, or something else altogether, increasing your income will improve many areas of your financial life, not just your DTI ratio.